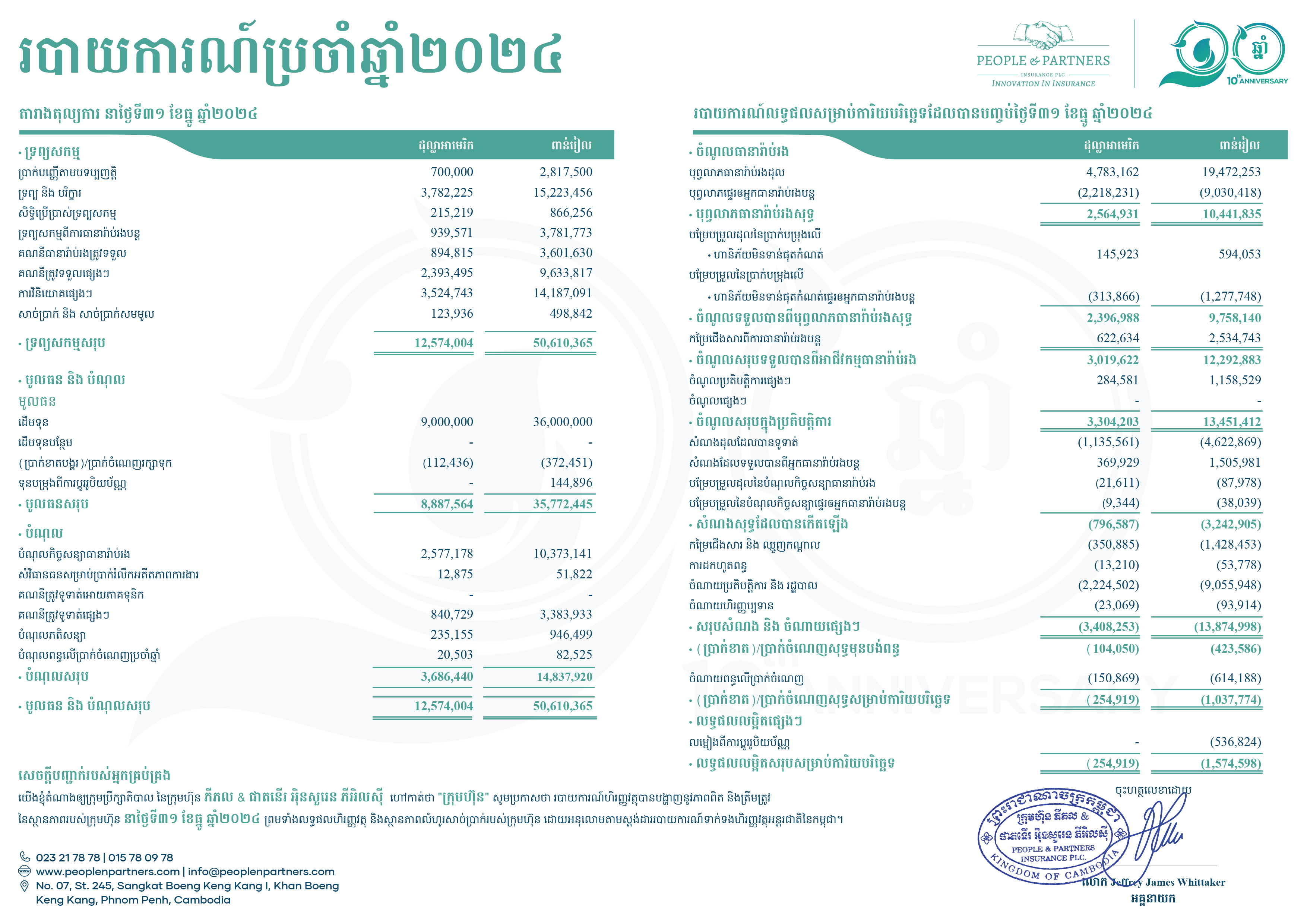

Jeff, when reading policy wording, I’ve seen ‘indemnity’ mentioned often but to be honest, I’ve never had a good understanding of what it is. You’ll see the term ‘Indemnity’ on policies all the time. It’s legal wording. It just means we agree to put you in the same position after the loss as you were before. No more, no less. You’re not allowed to make a profit. Of course, you’re always in a worse position after a loss. You have a fire, your belongings burn, you lose sentimental items and it guts you. We can put you in the same position, financially, but obviously we can’t compensate you for any emotional hardship.

|  |

There are different ways to indemnify. Cash payments are the most common type of indemnity. We can repair the item, and that’s common when clients have damaged their cars. If you’ve lost a specific model of car or motorcycle, we can offer you one exactly the same, if we want.

Sometimes we can do more than replace it. If you insure your house – the building for $100,000 and $50,000 for the contents – even though some of those contents may be old or worn, if you have reinstatement cover, we can reinstate it ‘as new’.

The type of indemnity – cash payment, repair, replacement, or reinstatement – varies according to what type of insurance it is and what kind of thing we’re indemnifying.

| You’ve only mentioned objects. What about accidents and life insurance? There’s a fundamental difference between an object and a person. You could insure your life for ten billion dollars because who’s to say what it’s worth? It’s priceless. If you lose an arm, your sight, or the use of your legs, who’s to say what it’s worth? What about David Beckham’s legs? Pianists can insure their fingers. But indemnity doesn’t apply to anything that involves insuring a person. The simple rule is: if it’s anything to do with a person (injury, illness or death) it’s not an indemnifiable thing. What are some of the more complex types of indemnity? Machinery and equipment are good examples that show how important this principle is. Can we find second-hand machinery to replace old machinery? If not, we may replace it with new machinery. We may look at the book value of the machinery. It depends. If you choose reinstatement when we create your policy, that’s okay, but you need to make sure you insure it for the right amount.

|

Liability Insurance also depends on the situation. The indemnity could be the amount of money awarded by the court but generally it’s better for everyone if we settle out of court. Someone may be asking for $3,000 and we know it would cost us $2,500 to go to court, so we just pay the amount they’ve asked for. The person who needs to be compensated is satisfied, our client is covered, and no one needs to get any lawyers involved!

For Marine Insurance, as we’ve discussed before, you don’t need an insurable interest until the time when you claim insurance because the value can change while the cargo is in transit. We normally pay for the cost of the cargo plus ten percent. We’ll over-indemnify you for Marine Insurance.

Because cargo is intended to profit once it reaches its destination?

Yes. We won’t pay you fifty percent above the cost of the goods, but we’ll pay ten percent. It’s fair. People think insurance is not fair, but this is a classic example of how we fall over ourselves to try and be fair.

What other factors affect indemnity?

Another way we can limit the amount of indemnity is, of course, a deductible – a self-insurance portion. Say you have a motorbike or a car, we may put a deductible on it, or you may agree to a deductible so you can get a reduced premium. When I go to the UK, I bear a $1,000 deductible.

So, you’re basically saying, I’ll handle anything up to a $1,000.

Yes, but in the case of a claim, an insurer will indemnify me, minus the $1,000.

That’s interesting. We talked about the case of the Twin Towers after the terrorist attacks, and the deductibles were huge.

Yes, sometimes they can be enormous, and in that case the deductible was many millions.

If I have a house insured, should I update the value insured?

You should do that about once a year. For a factory or a business, we make recommendations. To a factory owner, we may say, please review the sum insured. For a business, we may ask them to check their loss and profits. For instance, are you making 20 times more than you did last year?

According to the principle of utmost good faith, do you have a responsibility to remind clients?

We do, and we would ask a broker to ask their client to review the sum insured. It’s usually prominent on a bill notice.

But if you’ve got stock, is it manufacturer’s stock in trade? Is it wholesale or retail? We want to know which price you are insuring.

Like most principles applied to insurance, indemnity has a lot of factors and variables.

Indemnifying clients is not so easy to do, but we are always flexible. In most cases, the type of indemnity is tailored to the insured item. The aim is to get businesses back to work, and people back to their lives.

There are two more principles that only apply if the principle of indemnity applies. In other words, these two principles – subrogation and contribution – do not apply to insurances of the person. We’ll discuss those insurance principles next time.

Read the complete Principles of Insurance series: