- Home

- About us

- Products

- Blogs

- Join our team

- Contact

- Download

-

Others

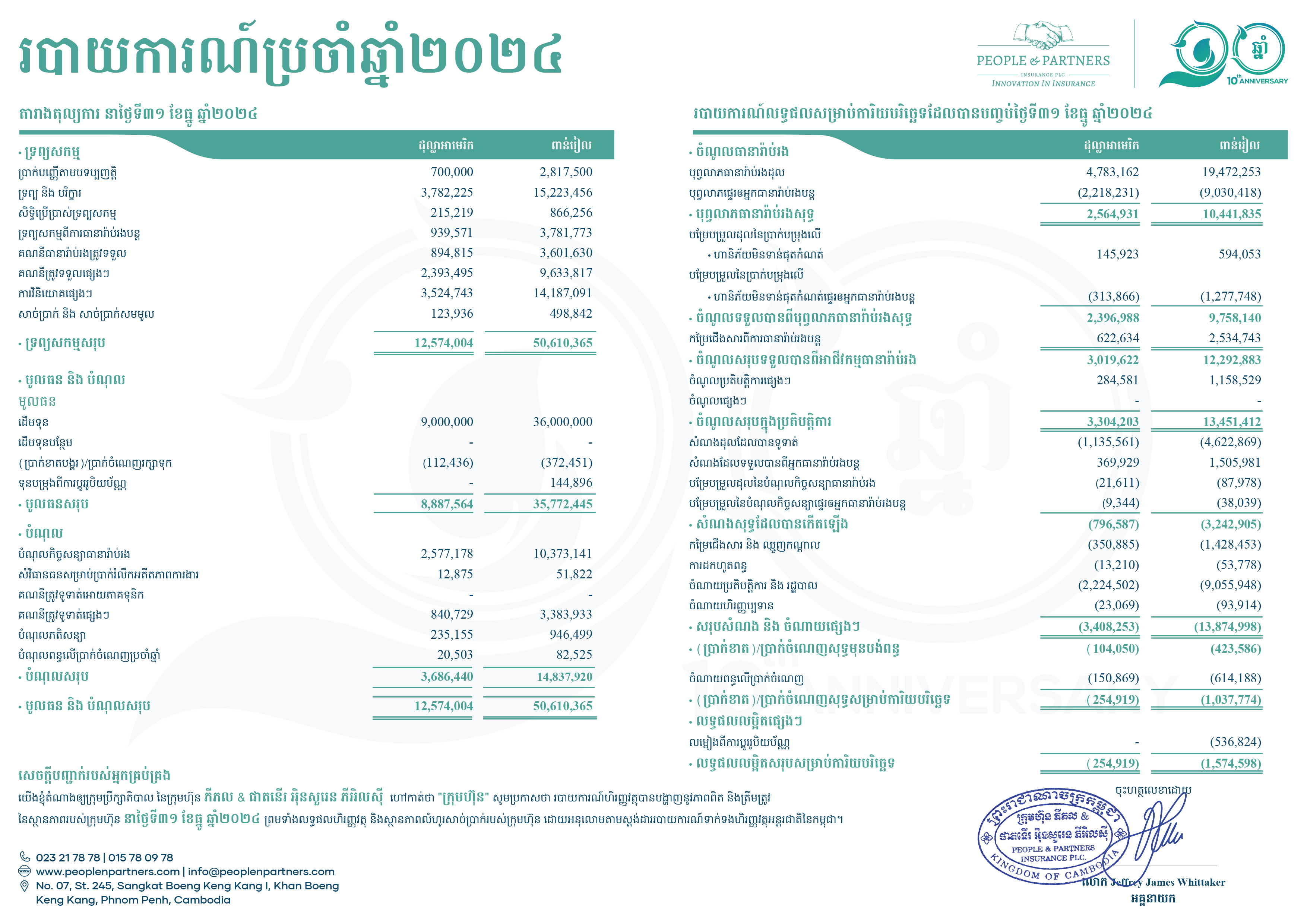

Annual Report

A Decade of Excellence. A Future of Innovation.

Verify Insurance Policy By National Id CardEnsure accuracy in your motor and healthcare insurance details by simply scanning your national id card .

Motor Insurance Quotation EstimatorEasily get a motor insurance quotation by uploading your vehicle registration card or entering basic information.

Verify Your Motor InsuranceEnsure accuracy in your motor insurance details by simply scanning your vehicle registration card.

Panel & Garage LocatorFind all of our partnership locator.

Panel clinicsFind all of our partnership clinics in Cambodia.

Repair GarageFind all of our partnership repair garage in Cambodia.

Claim complaintsFile a claim complain.

Legal & ComplianceDiscover our comprehensive legal and compliance standards, designed to ensure a trustworthy environment

Claims FormFor claiming your insurance, please find the claims form here.